Source: Business economics, higher education at Jørgen Waarst and Knud Erik Bang

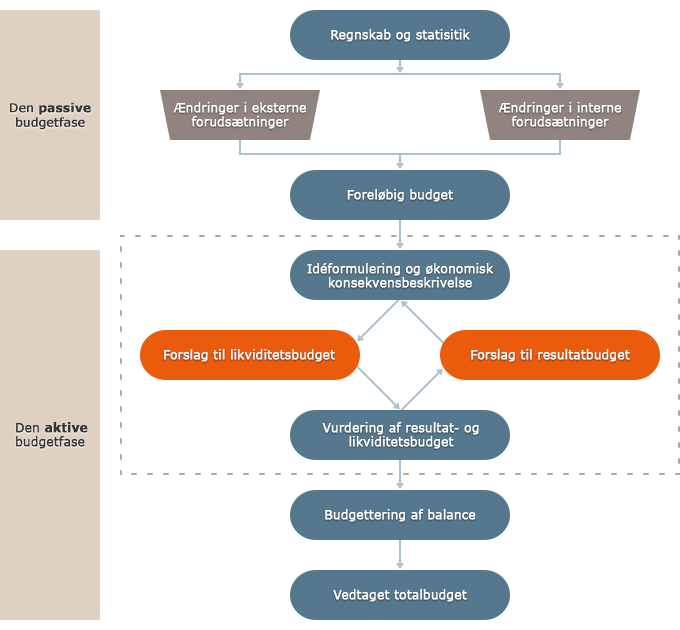

The passive budget phase:

The accounts show how the past period went. In the passive phase, the past is projected with an unchanged course of action, incorporating both internal and external preconditions.

The starting point for the first budget phase is therefore the just completed accounts. It expresses the financial consequences of the actions that were the basis of the previous budget. Through the accounts, you can see about the effort, i.e. hiring, development and investments, had the expected effect in relation to the objective the company was working towards. The result of this can be read in the organization that has been built as well as the values and debts that are reflected in the balance sheet. Precisely these elements will be the starting point for the coming budget year.

The completed accounts will therefore form the framework for the upcoming budget. But since there are changes in internal and external factors, one cannot of course expect to be able to repeat the same actions in a new year with the same results. Therefore, you have to adjust your expectations to the new economic conditions.

Changes in the internal conditions can be expressed in the form of:

- a marketing campaign carried out in the past year, but which will also have an effect in the coming budget period.

- Investments made in new and more efficient machines that can affect the contribution margin.

- Development and launch of new products.

- Agreed wage adjustments

Changes in external conditions can be:

- New legislation that affects / imposes increased burdens on the company on working conditions, environmental conditions and tax conditions.

- Changes in the overall economy can have an impact on the company's customers, expressed in terms of the customers' purchasing power / desire.

- Newly developed technologies / products can shift customers' focus in a new direction.

- New customer focus automatically leads to a changed competitive situation.

- Factors such as company acquisitions / mergers among competitors will also have a consequence, because of the competition the company will face in the new year.

- A changed interest rate level will be reflected in the company's financing costs.

- Changed prices of raw materials as a result of international trade. Eg. increasing on oil, steel, copper, foodstuffs etc.

The passive budget phase ends with the company, on the basis of the above, preparing a preliminary budget, in which the changes in the outside world that can be identified are incorporated into the final accounts.

The active budget phase:

Based on the preliminary budget, the active budget phase is about looking at the opportunities available to improve the company's future earning potential.

In other words, the active budget phase is about investigating whether the action plans that have formed the basis for the company's development until now are now also the best for the company's future development or whether changed conditions in the company's environment make it possible to get an even better result of an adjustment of the action plans.

It is also an opportunity to brainstorm around different scenarios, to test whether there is a basis for giving the company increased earnings or improved liquidity.

The phase is popularly called 'To screw up the 4 P's' – Price, Product, Place and Promotion – (price, products, markets and marketing). Below are a number of examples of questions that should be clarified in this phase

- Would it be beneficial for us to sell product A for 25 % more?

- Would it be beneficial for us to phase out product C and phase in product D?

- Will a relocation of production be profitable?

- Should we sell product K in Russia?

As a result of this phase, you get a profit and liquidity budget, which must be tested against the company's overall goals.

The active phase is repeated until the goals are reached, and a finally agreed profit and liquidity budget and a derived balance budget can be made.

Read more about liquidity budget

Read more about balance budget

This material contains a processing of the Audit of Finance for Managers developed for the Ministry of Education by the Continuing Education Committee for Trade, Administration, Communication and Management in collaboration with Britta Slot Johnsen, Søren Peder Lauridsen, Bjarne Wølch Rasmussen and Henrik Strømkjær.